Don’t Count Peloton Out. It’s Just Getting Started.

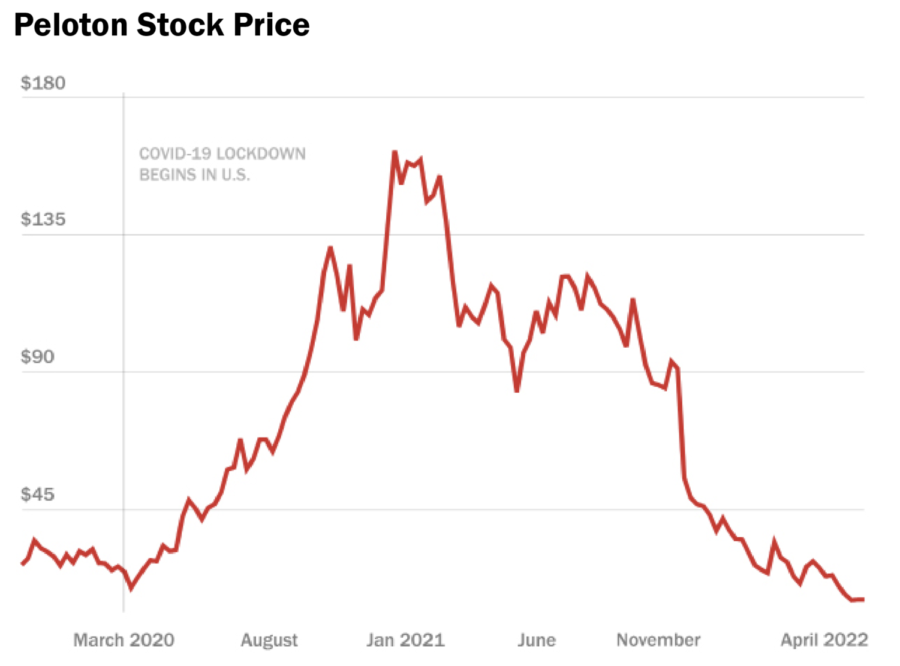

During the pandemic, Peloton, an at-home tech and fitness company, soared in value. Although it certainly had a large dip in usage and revenue post-pandemic, I believe that Peloton’s value will rebound as soon as this fall.

During the initial self-isolation period of the pandemic, people were unable to go to the gym and work out normally; as a result, Peloton’s app subscription service, which allows people to follow live workout sessions with verified trainers from the comfort of their homes with minimal equipment, began to take off. However, as in-person establishments started to reopen, and people were able to go back to gyms in person, usage of the app declined drastically. In fact, it is estimated that the number of daily users on the app from April to September of 2021 dropped by over 42%. During the pandemic, people were willing to pay a premium for Peloton’s services, but as things started to reopen, this was not the case.

Furthermore, Peloton’s 8-K form filings (as viewed from the SEC) were even more telling of their imminent downfall. In their quarterly 8-K filings, Peloton filed their quarterly shareholder’s letter; in which they exhibited their quarterly total revenue. From that data, it is clear that as the pandemic started in 2020, there was a sharp increase in revenue, from 223.3 million to 466.3 million from Q4 2019 to Q2 2020. This increase continued to be seen into Q2 of 2021 as the quarterly total revenue jumped to 1,064.8 million, and then reached its peak in Q3 of 2021 at 1263.3 million. However, as everything was truly starting to reopen at this time, vaccines were rolling out at high rates, and masking policies were relaxing, there was a steep decline in the quarterly total revenue. In Q4 of 2021, it dropped to 936.9 million, and then in Q1 of 2022, it dropped to 805.2 million.

As time went on, Peloton’s user base dropped significantly, causing a massive correction in the share price. While researching stocks for a stock trading game, I saw that Peloton stock had essentially crashed, having dropped by over $120 a share from what I had seen it at during the early pandemic. After spotting this, I assumed it was on its downfall.

In addition, Peloton’s trailing P/e (price/equity) ratio from 2021 is far from ideal. Peloton had a P/e of 154.07, which is very high. In comparison, the S&P 500 typically has a P/e ranging from 13-15. The P/e ratio compares a company’s earnings to share price, and a high P/e ratio generally means that a company is overvalued. Given that Peloton’s is so high, that is a strong sign that it was very highly overvalued. This proved to be true, as Peloton continued to sharply drop. What was interesting, however, was Peloton’s beta value: the fact that its beta value was 0.96, which is below 1, indicates that it is not volatile, and offers steady returns. I was confused by this value, as I had seen Peloton’s share price sharply increase and then sharply decrease over a two year period (2020-2022) by hundreds of points.

As mentioned earlier, I do believe that, in the near future, Peloton is going to make a shift and a move back up, rather than continuing to fall. I estimate this to begin to happen latest by Q4 of 2022. I do not believe that it will reach its mid-pandemic height; however, I think that it will at least double its current value. The reason for this is twofold. Firstly, in its Q2 2022 Shareholders Letter, Peloton shared data that displayed both its quarterly total revenue and its subscriber count being on an upward trend.

In the shareholder’s letter, Peloton stated that it was in the process of building its first factory for fitness products in the USA, and hopes to have completed construction by 2023. By creating a factory within the USA, the hope is that production lines should be shortened, and production should also be cheaper. This would also aid with sales, as production would be much faster and shipping would as well. This means that customers can get their product sooner, and are more likely to buy from Peloton.

Furthermore, a report published by the SEC showed that John Foley, a Chief Executive at Peloton, bought options to purchase shares of Peloton stock, which shows that those in positions of power and influence within the company still believe in the company. The confidence of Peloton insiders signals the possibility of a strong financial showing in the near future for Peloton.

Peloton’s financial data, the news of Peloton’s first factory in the US being built, and John Foley’s buying options to purchase shares of Peloton stock all signal that the company is rebounding. It will be interesting to see the Q3 2022 Shareholders Letter to see if the quarterly total revenue continues to increase, or if Q2 2022 was an outlier in what is going to be a consistent decline into Peloton’s ultimate demise. I strongly believe in Peloton as a company and think that it will make a return.